Stability Metrics

Stability metrics evaluate price consistency and volatility over time. They quantify the risk that a token's value will move adversely, reducing collateral quality or triggering liquidations.

Metrics Reference

Stability Ratio

The ratio of the lowest price to the highest price over a rolling window.

Stability = low / high

Volatility proxy = 1 - Stability = (high - low) / high

A Stability Ratio of 0.90 means the asset traded within a 10% range. Values approaching 0 indicate high volatility. Used as a quick volatility proxy when full time-series data is unavailable.

Alpha Score

Measures how long a single entity maintains market leadership across a group. Computed as:

Alpha Score = days_in_leadership / total_days

A network or pool that leads in volume for 67 out of 100 days has an Alpha Score of 0.67. High Alpha Scores indicate persistent dominance — structurally important venues whose failure has outsized impact.

Value at Risk (VaR)

The maximum expected loss at a given confidence level and time horizon, modeled using Monte Carlo simulation. Bitpulse computes both Collateral VaR and Loan VaR across multiple time horizons (1-day, 7-day, 30-day).

Supported models:

- GBM (Geometric Brownian Motion) — standard baseline

- GBM+VIX — volatility-adjusted using the VIX index

- GARCH — captures volatility clustering (heavy tails)

- Historical — replays actual price path distributions

See the Risk API — VaR endpoint for full parameter reference.

Conditional Value at Risk (CVaR)

The expected loss given that a loss exceeds the VaR threshold. Also called Expected Shortfall. More conservative than VaR — captures the severity of tail events, not just their probability.

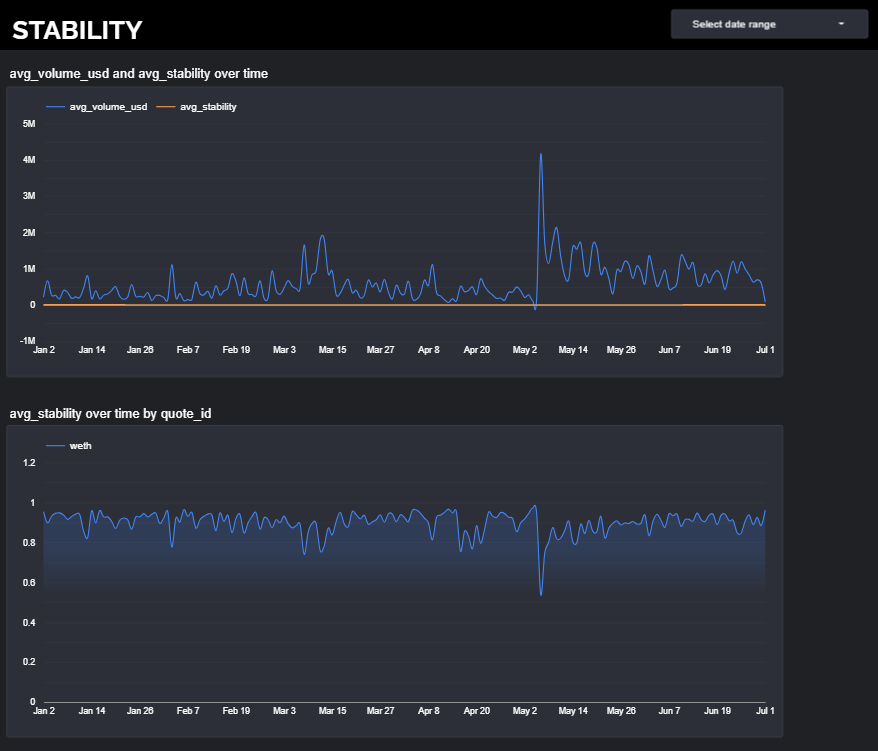

Example dashboard: