Loan Margin Optimizer

The Loan Margin Optimizer is a powerful pre-trade tool integrated into our client portals that helps institutions calculate and find optimal collateralization values for new loan positions.

Purpose & Functionality

This calculator is designed to be leveraged at loan origination stages to create optimized loan structures that achieve very specific risk probability percentages for liquidations and margin calls, based on user-defined Risk Profiles and tolerance levels.

The model takes a comprehensive set of inputs and converges toward optimal collateralization ratios within specified lower and upper bounds to yield the desired risk probability (e.g., a 2% "Probability of Liquidation").

Key Features

- Risk Profile Optimization: Target specific risk probabilities for new loans

- Monte Carlo Simulations: Generate predictive risk probabilities using advanced statistical models

- Multiple Model Options: Choose from GBM, GBM with Deribit Implied Vol, or Historical data models

- Comprehensive Parameter Control: Fine-tune all aspects of the risk simulation

Input Parameters

Risk Profile Settings

- Optimization Target: The variable to be optimized (currently supports Probability of Liquidation)

- Target Probability: The desired risk probability target

- Error Tolerance: Acceptable deviation from the target probability

- Lower/Upper Bounds: Min/max values for the resulting Initial Collateralization Ratio

- Liquidation Collateralization Ratio: The liquidation threshold for the position

- Margin Call Top Up Time: Grace period between margin call and top-up requirement

Model Settings

- Model Type: Choose from GBM, GBM Deribit Implied Vol, or Historical

- Monte Carlo Iterations: Number of simulation runs (e.g., 10,000)

- Model Lookback: Historical data window for model calibration

Position Settings

- Principal Asset(s): Loan assets with optional weighting for diversified loans

- Collateral Asset(s): Collateral assets with optional weighting

- Initial Collateralization Ratio: Starting collateralization level

- Position/Loan Size: Value in USD to be loaned

- Position/Loan Duration: Term of the loan in days

- Margin Call/Liquidation/Recovery Ratios: Risk thresholds for the position

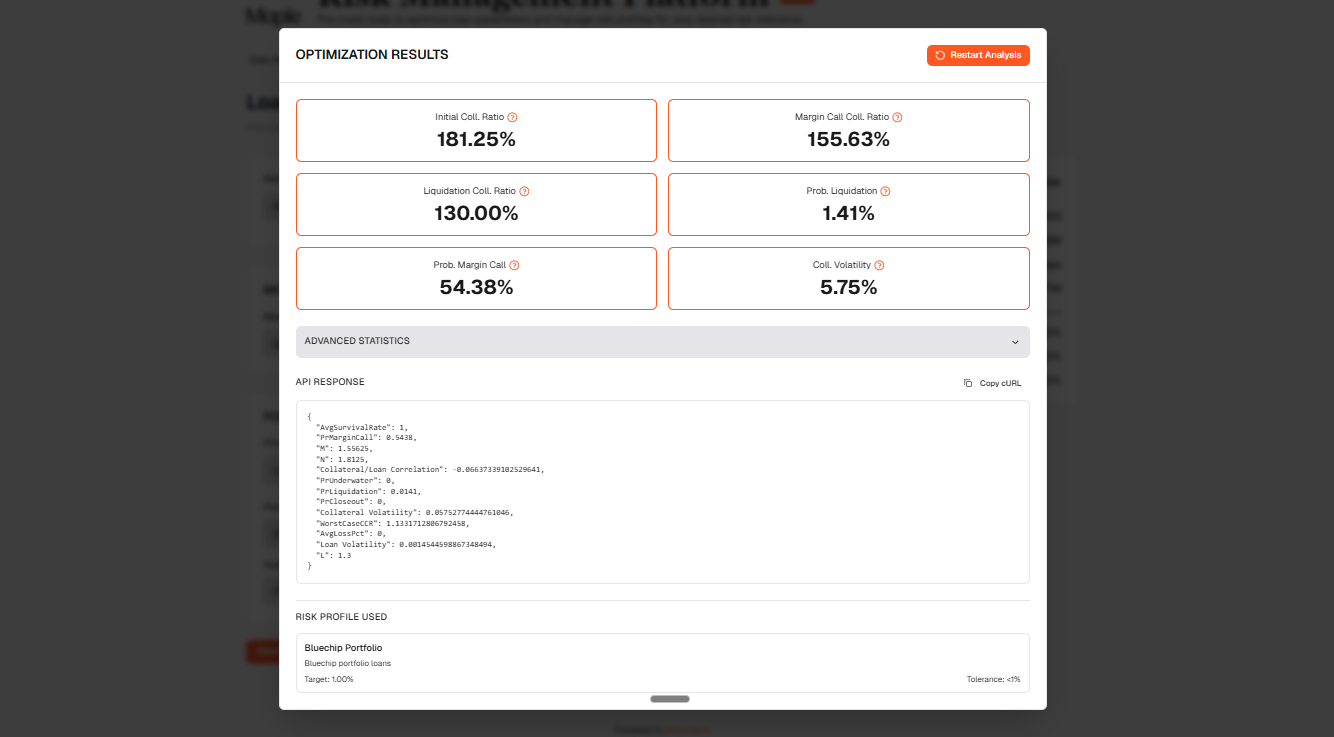

Outputs

The Loan Margin Optimizer provides comprehensive risk metrics including:

- Optimized Initial Collateralization Ratio: The ideal starting collateralization level

- Margin Call Collateralization Ratio: Optimized margin call threshold

- Probability of Liquidation: Risk of hitting liquidation threshold

- Probability of Margin Call: Risk of hitting margin call threshold

- Average Loss Percentage: Expected loss in case of adverse events

- Average Survival Rate: Expected loan performance metric

Integration Options

This tool can be customized to match your institution's specific risk parameters, collateral types, and risk tolerance levels. It integrates seamlessly with other components in your client portal for a comprehensive risk management solution.